The response was overwhelming this fall when news broke that Fannie Mae and Freddie Mac were working to make President Trump's 50-year mortgage loan plan a reality.

Personal finance experts and housing market analysts called the idea terrible. The interest accrued over half a century would be astounding, they said. Meanwhile, amping up the buying power of millions of Americans would inflate home values.

Within a week, the Treasury department backed off the idea.

All this negative talk got us thinking more about the positive aspects of 50-year home loans and how home buyers might benefit from longer terms without paying their high costs.

First, what exactly is a 50-year mortgage?

Back in 1934, the 30-year mortgage put home buying within reach of millions of Americans, allowing for lower payments and fixed rates. The 30-year mortgage remains the most popular way to finance a house.

A 50-year mortgage would stretch a home loan across 20 additional years, requiring 600 monthly payments, dwarfing the standard 360-payment model the 30-year loan requires.

The big advantage for buyers: lower monthly payments on the same home price. Rather than paying, say $1,600 a month to buy a $250,000 home, a buyer might pay $1,300 a month.

These are rough estimates. Prices for real buyers vary by credit score, debt-to-income ratio, and other unique factors. But the logic holds: Spreading debt across more time lowers debt payments.

The pros and cons of 50-year mortgages

Lower monthly payments, but at what cost? Let’s take a closer look at the pros and the cons of 50-year mortgage loans. First, a closer look at the positives.

The good: About those lower payments

Payments on a $400,000 loan at 6 percent would look something like this:

| Loan Term | Monthly Payment |

|---|---|

| 30 years | ~$2,398 |

| 40 years | ~$2,266 |

| 50 years | ~$2,105 |

For example purposes only. These estimates include principal and interest only. Real payments would also include property taxes, homeowners insurance, mortgage insurance, and HOA fees as applicable.

This 50-year loan saves almost $300 a month in this example compared to the standard 30-year loan’s payments.

But so what? With payments already north of $2,000 a month, not including taxes and fees, $300 doesn’t seem like much of a windfall.

For buyers on the cusp of loan approval, that $300 could make all the difference. It could:

– Push the buyer off the fence into eligibility range for a median-priced home

– Compensate for the business deductions that lower documented income for self-employed borrowers

– Put buyers with higher-than-average debt into the market for becoming homeowners

The advantages of a 50-year loan are clear. What about the downsides?

The bad: The cost of paying less per month

Regardless of their loan term, a home buyer should always know the long-term interest costs they’re signing up for. For a 50-year loan, those costs, over the life of the loan, would be a lot higher than the interest paid over 30 years.

Let’s go back to our $400,000 loan at 6 percent to see the difference:

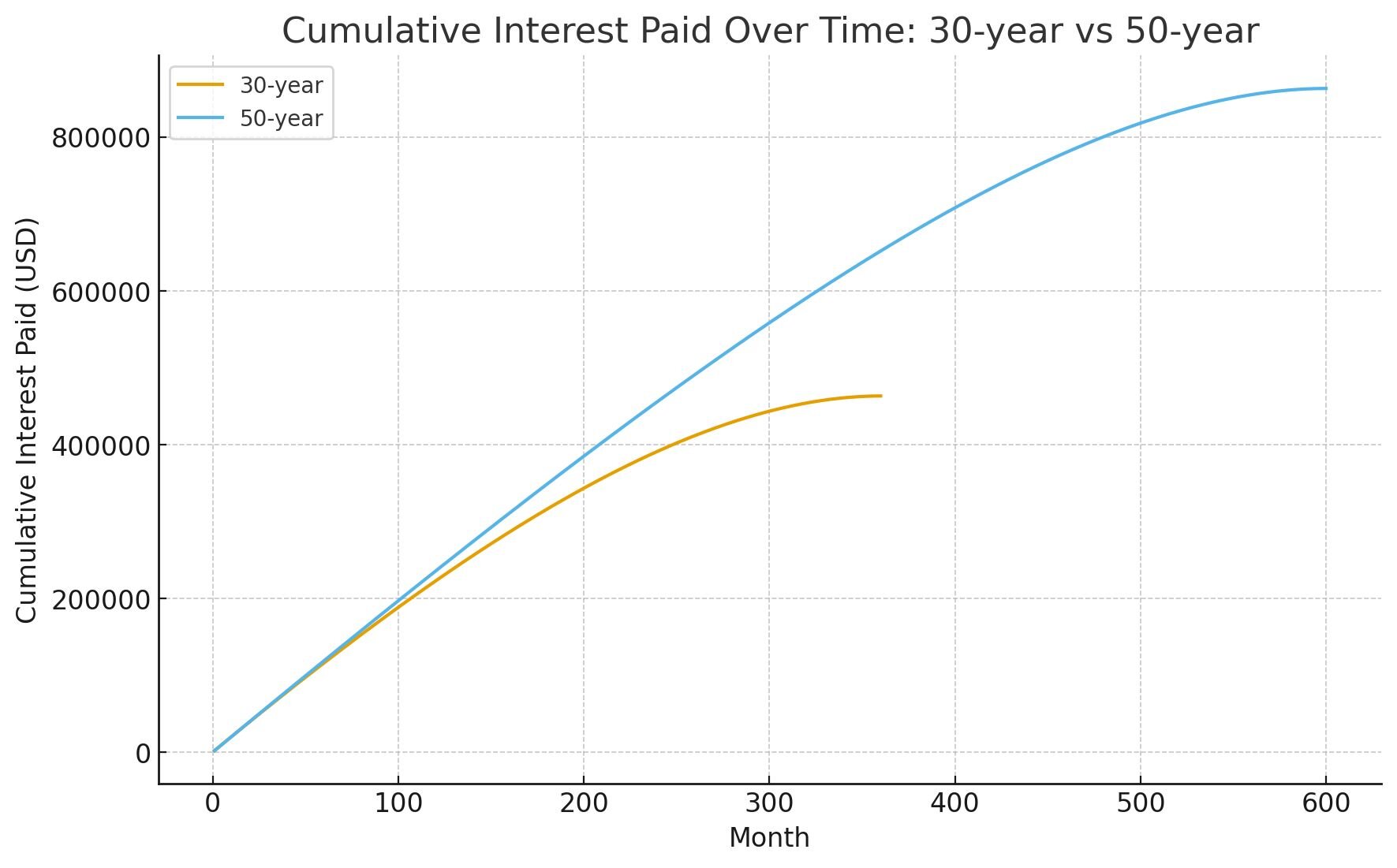

- 30-year mortgage: ~$463,000 interest over the life of the loan

- 50-year mortgage: ~$863,000 interest over the life of the loan

Those numbers speak for themselves. Repaying the same $400,000 over 50 years adds another $400,000 to the price of the $400,000 home. The borrower would effectively pay for the home all over again during the last 20 years of a 50-year term.

More bad about all that interest

The additional interest paid on a 50-year term goes deeper than the price tag. The extra interest slows the growth of home equity, which means the loan builds wealth for the buyer at a slower pace.

Here are the first 12 payments of the 50-year loan we’ve been using as an example:

| Month | Payment | Interest | Principal | Loan Balance |

|---|---|---|---|---|

| 1 | $2,105.62 | 2,000.00 | 105.62 | 399,894.38 |

| 2 | $2,105.62 | 1,999.47 | 106.15 | 399,788.23 |

| 3 | $2,105.62 | 1,998.94 | 106.68 | 399,681.56 |

| 4 | $2,105.62 | 1,998.41 | 107.21 | 399,574.34 |

| 5 | $2,105.62 | 1,997.87 | 107.75 | 399,466.60 |

| 6 | $2,105.62 | 1,997.33 | 108.29 | 399,358.31 |

| 7 | $2,105.62 | 1,996.79 | 108.83 | 399,249.48 |

| 8 | $2,105.62 | 1,996.25 | 109.37 | 399,140.11 |

| 9 | $2,105.62 | 1,995.70 | 109.92 | 399,030.19 |

| 10 | $2,105.62 | 1,995.15 | 110.47 | 398,919.72 |

| 11 | $2,105.62 | 1,994.60 | 111.02 | 398,808.70 |

| 12 | $2,105.62 | 1,994.04 | 111.58 | 398,697.13 |

As you can see, the $25,267 spent on loan payments during the first year paid down the loan balance by only about $1,300. The original $400,000 loan balance is down to about $398,697.

Equity growth accelerates each year, as more of each payment goes toward the loan’s principal, but equity still grows at a glacial pace during the first five to seven years of the loan.

A 30-year loan also starts slow, but equity growth gains traction sooner, typically within the first three years of the loan term.

This graph compares amortization progress in a different way.

Could 50-year borrowers harness the good without paying the bad?

In a nutshell, more people could qualify for a 50-year loan because of the lower payments, but the costs of the loan run higher as time passes.

So here’s the key question: Could a buyer harness the good (the lower payments) without experiencing the bad (paying the excessive long-term interest costs)?

The answer to that question, for some buyers, is yes. A home buyer, for instance, could keep a 50-year loan for two or three years. Then, they could refinance the debt into a shorter term, maybe a traditional 30-year fixed. By then, maybe they’d earn more income, have less debt to deal with, or interest rates may be lower.

A positive 50-year mortgage scenario

Let’s return, once again, to that $400,000 loan we used above. But instead of borrowing at 6 percent, the home buying family in this example gets a rate of 8 percent because their debt-to-income ratio pushes the limits of eligibility.

Principal and interest payments on this 30-year loan would be almost $3,000 a month, too much for this family to qualify for. This family will need to look for a cheaper home, in a neighborhood where prices have been stagnant, or keep renting a few more years while they pay off debt.

Except, in this imaginary scenario, a 50-year mortgage exists, and the family’s loan officer brings up the idea. Pushing the loan term to 50 years gets that payment down to about $2,710. This makes a difference. The family qualifies for the loan and can become homeowners.

The 50-year loan in this scenario was always temporary

Over the first two years of the loan, this family is able to make all 24 on-time payments, getting the original $400,000 loan balance down to $397,500. They’ve hardly made a dent in the loan balance.

But during those two years, their financial situation changed. They paid off their car and lowered their credit card debt. Both spouses got raises at work. Plus, the home they bought appreciated. It’s now valued at $425,000.

Now, they can qualify to refinance their $397,500 debt over 30 years at 6 percent. The principal and interest due on this loan is $2,383 a month, much lower than the $3,000 a month they would have been paying if they’d gotten into a 30-year loan two years earlier.

Plus, their new 30-year loan saves $220,000 over the life of the loan compared to what they would have paid on a 30-year fixed two years earlier if they had been able to get approved.

And, they’re not chasing higher home prices. Since getting their foot in the door with the 50-year loan, they have benefited from the rise in home values. Their higher home value helps lower the interest on the new refinance loan.

Other ways to lower payments temporarily

We know real life won’t always follow the ideal scenario above, in which the home buying family used a 50-year mortgage to their advantage. In real life, borrowers could lose a job, take on more debt, or face a more volatile market for rates in the future.

In real life, a borrower might get stuck paying a 50-year loan’s higher interest charges for two more years. And this scenario doesn't address the fact that 30-year and 50-year loans wouldn't charge the same interest rate.

But the idea of using a mortgage temporarily isn’t unique to 50-year loans. In fact, buyers have been doing this for decades with:

Adjustable-Rate Mortgages (ARMs)

ARMs almost always offer lower initial rates than fixed-rate loans. The initial rate is often 0.5% to 1% lower than a comparable fixed mortgage, lowering payments and helping more buyers qualify.

In exchange for this lower rate, the borrower risks paying a higher rate later, once the loan’s initial rate period expires and the loan starts floating to match market conditions.

But many home buyers plan to refinance into a fixed-rate loan before their ARM starts fluctuating. And if they can't refinance, modern caps on ARMs keep rates from going off the rails.

Like 50-year loans, the goal is to use ARMs strategically.

Interest-only mortgages

Interest only, or IO, loans require only interest payments during the first five to 10 years of the loan’s term. This sounds dangerous, but when you consider how little principal gets paid down during the first years of a traditional loan anyway, paying nothing on principal seems less risky.

But there is plenty of risk: IO loans may charge a balloon payment once the interest only period ends. This means the entire balance would come due at one time, making a refinance essential for most buyers.

Investors who plan to rearrange their portfolios or sell other real estate before the balloon payment comes due tend to like this kind of financing. It saves money, temporarily, while they make other arrangements. Most primary residence buyers, however, should avoid IO loans since the balloon payment could cause a lot of stress.

How other countries have used 50-year loans

Longer mortgage terms aren’t unique to the U.S. in the fall of 2025. Several countries use or have experimented with them, including Japan, the U.K., and parts of Europe.

Japan: multi-generational mortgages

Japan introduced 50- and even 100-year mortgages during the real estate boom of the 1980s. These loans have been passed from parents to children. These loans reduced stress in massive housing markets like Tokyo where buying had become almost unreachable.

United Kingdom: 40- and 50-year mortgages

Some lenders in the U.K. still offer 40- and occasionally 50-year mortgages to help younger buyers afford property in bustling cities like London.

What these countries learned

- Longer terms did make buying possible for more renters

- Longer terms also drove up home prices because all buyers could borrow more

Based on these examples, longer term mortgages can solve a short-term problem but can create long-term risks if they become widespread.

Scaling the good vs bad in 50-year mortgages

Like all financial products, a 50-year mortgage would introduce risk and reward into the market.

Ultimately, what’s good and bad about a loan product for individual home buyers can be scaled up as strengths and weaknesses for the entire housing market.

If Fannie and Freddie decided to allow longer term mortgages, such as a 50-year loan, the loans should be used temporarily and strategically and not as a reason to inflate housing budgets unnecessarily.

See your rates on today's 30-year loans

50-year loans don't exist in the U.S. For now, most buyers can max out their loan terms at 30 years.

You could see how much you could afford with today’s 30-year loan terms by experimenting with a mortgage calculator.

Market interest rates set the context for your interest rate, but within that context, your personal finances make a big difference.

You can see how your unique personal finances affect your home buying budget with a preapproval.

...in as little as 3 minutes – no credit impact

All figures in this article are illustrative and not offers or commitments to lend. Actual rates and terms depend on underwriting and market conditions.