What you'll learn ✅

- Where mortgage rates stand today and what moved them

- What the March jobs report means for rates going forward

- Whether to lock your rate now or wait

- When refinancing makes sense given today's environment

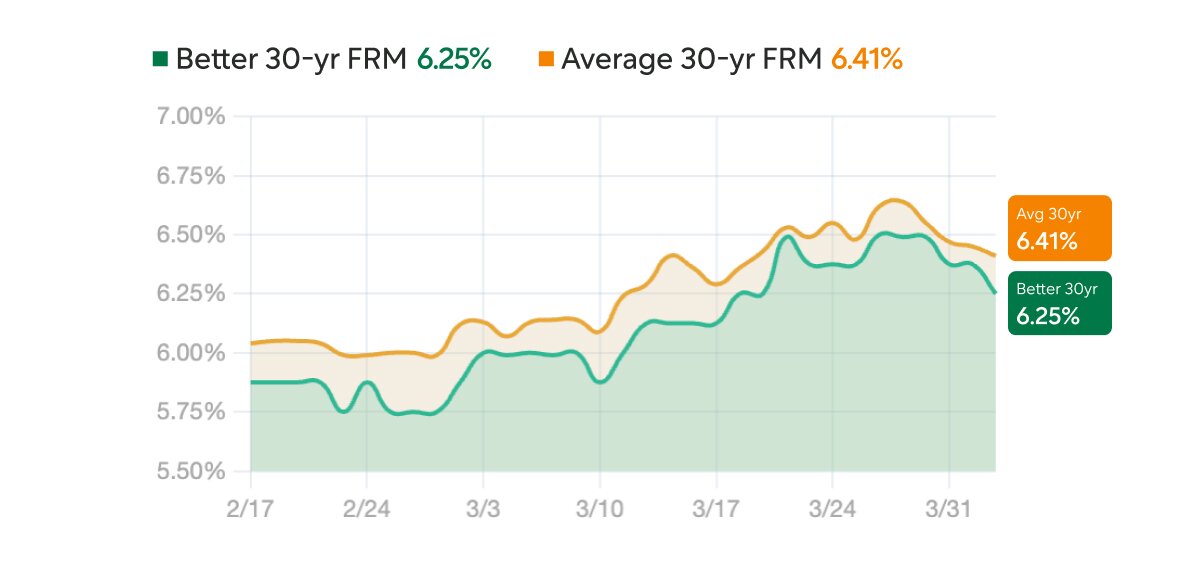

Mortgage rates edged lower on Friday, April 3, 2026 — though not dramatically. The 30-year fixed-rate mortgage is averaging around 6.31% today, down slightly from yesterday and about 14 basis points below last week. A basis point is one one-hundredth of a percentage point, so this is a modest shift, not a turning point. If you're waiting for a major drop before moving, that's a gamble right now — and one with real costs if rates move the other way.

Rates shown are daily average interest rates, not APRs, based on Better Mortgage data and are for informational purposes only. Rates are not guaranteed, may include borrower-paid or lender credits, and actual rates and terms vary by borrower and transaction. Comparison to Mortgage News Daily averages may not reflect individual borrower scenarios and is not a guarantee of lower rates or savings.

No commitment required. Check your rate without affecting your credit score.

What moved rates today

The March jobs report came in far stronger than expected — 178,000 new jobs versus a projection of just 59,000. Strong employment data usually pushes rates higher, not lower, so the slight dip today reflects competing market forces, particularly volatility tied to oil prices and the ongoing conflict in Iran.

Mortgage markets are closed on weekends, so today's rates are unlikely to shift until Monday. The bigger moves will come next week, when two key inflation reports — the February PCE and the March CPI — are released. If those numbers show energy prices feeding into broader inflation, expectations for Fed rate cuts this year will likely fade. That makes locking in a rate you can afford today a more disciplined move than waiting on data you can't predict.

You can track current mortgage rates and what determines mortgage rates to stay informed as conditions evolve.

Should you lock your rate or wait?

If you're in contract and your closing is coming up, confirm your rate lock timeline now. Most locks run 30 to 60 days, and with this much volatility, an expired lock is a real risk.

If you're still early in the process, use this time productively. Your credit score, debt-to-income ratio, and down payment all affect the rate you'll qualify for — and those variables are more within your control than what happens at the next Fed meeting. You can also use our mortgage calculator to stress-test different rate scenarios against your budget.

The broader question of is now a good time to buy a house depends heavily on your personal finances, not just where rates are on any given Friday. If today's rate produces a payment you can comfortably afford, that's the clearest signal to move.

Is refinancing worth it right now?

Refinancing generally makes financial sense when you can reduce your rate by at least 0.5 to 0.75 of a percentage point — and when you plan to stay in the home long enough to recoup the closing costs. At today's average, that means homeowners sitting at 6.8% or higher are worth looking closely at their options.

This varies by loan size and remaining term, but the savings potential is real for borrowers who locked in during the 2023–2024 rate spikes. Use our refinance calculator to run your own numbers, or read up on when to refinance your mortgage for a more complete framework.

If your goal is accessing equity rather than lowering your rate, a cash-out refinance or HELOC may be a better fit. Those are different products with different cost structures — worth understanding before you decide.

Better rate-and-term refinance customers save an average of $999 per month.¹

Disclosures

¹ Based on internal analysis of Direct-to-Consumer rate-and-term refinance loans funded by Better Mortgage between January 1, 2025 and October 31, 2025. Savings amounts represent an average across this population and do not reflect a guaranteed or typical result. Individual savings will vary based on loan terms, interest rate, credit profile, property value, loan amount, and market conditions. Monthly payment figures shown reflect principal and interest only and do not include taxes, insurance, HOA dues, or other applicable costs, which may increase the total monthly payment. Not all borrowers will experience monthly savings, and refinancing may increase total interest paid over the life of the loan.

Additional Rate Details:

Rates shown are daily average interest rates (not APRs) based on Better Mortgage data and are for informational purposes only. They may not reflect the rate you qualify for. Actual rates and terms vary based on credit profile, loan characteristics, property type, and market conditions.

Comparison is based on Better Mortgage average rates versus Mortgage News Daily (MND) national averages for a 30-year fixed-rate mortgage during the period Feb 17 – Apr 2, 2026, using a representative loan scenario (e.g., ~$523,000 loan amount), which may not reflect all borrower situations. Differences may reflect data methodology, timing, and borrower mix and are not a guarantee of lower rates or savings.

Rates are subject to change without notice and are not guaranteed. This is not a commitment to lend. Additional terms and conditions apply.